tmrw

Good Market, Bad Advice

Oct 30, 2025

Life is good, but hard.

Over the past few months, my team and I have spoken with many of you. It has been amazing to hear your stories, inspiring to learn about your dreams, and at times, heartbreaking to hear about the setbacks.

One thing keeps coming up again and again, and our data from new readers backs it up:

Many of you are not satisfied with your financial advisor.

Here’s what you’ve told us:

No real or reliable financial plan

Inconsistent communication

Investment losses you don’t understand

Being moved around to different advisors like hot cakes

All while living through one of the best bull markets of all time.

Here’s what the data shows from June:

More than half of those who currently work with an advisor say they aren’t fully satisfied.

So today, I want to talk about how to choose a financial advisor.

This isn’t about convincing you to hire Fjell or to fire your current advisor.

My goal is to share what I’ve learned after nearly 12 years in wealth management and to help you confirm what you may already be feeling.

Great advisors can be worth their weight in gold. They can do incredible work. You want to find one of them.

Here’s what they look like.

People hire financial advisors to solve problems they either cannot do themselves or do not want to do themselves.

It’s nothing more complicated than that.

Usually, there is an immediate problem that needs to be addressed, which kick-starts the relationship, and things evolve from there.

Here are a few of the problems we have helped clients solve over the past six weeks:

Funding real estate purchases

Transitioning businesses

Placing alternative investments

Planning for 2026 taxes

Setting up 529 plans for children/grandchildren

Designing charitable giving strategies

Investing in artificial intelligence

A good advisor helps you make sense of the specific challenges you face and helps you get ahead of them, not just react to them.

From my perspective as a financial advisor, when you hire a professional service, whether it is a primary care doctor, CPA, estate planner, or financial advisor, you are buying execution and expertise first. But the long-term success of that relationship depends on trust.

As you know, relationships either build or destroy trust over time.

When trust is high, honest and productive conversations can happen. That is when meaningful financial progress takes place.

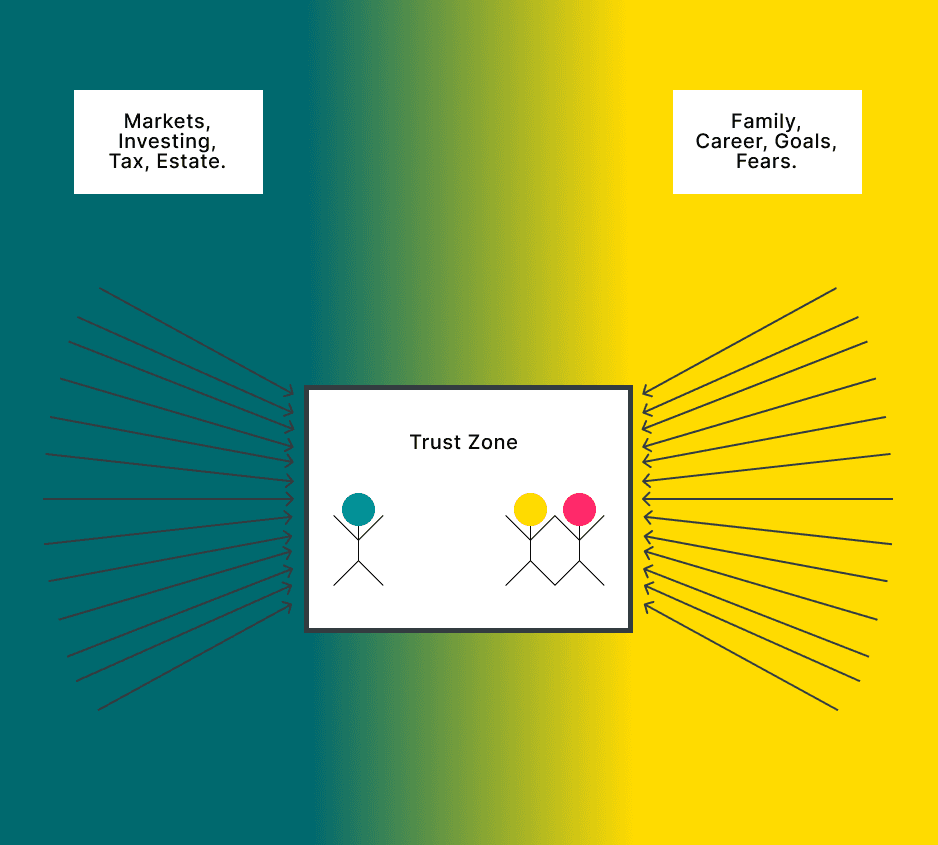

Here’s a picture of how I have always viewed my role as an advisor:

The Trust Zone, and the constant pressures on it.

There are two main components in this graphic: the blue area and the yellow.

The blue represents the world where you invest, work, and live. Think tax law changes, market declines, asset allocation strategy, the economy, and investment selection.

The yellow represents your world. Your family, your dreams, your fears. Think, “I need to understand what a nursing home stay means for my wife and me,” or “When should I retire, and what happens if I get laid off in two years?”

When those two forces push together, you get the place where your financial life truly lives. Let’s call it the Trust Zone.

The arrows represent all the good and bad inputs that are constantly trying to influence your financial decisions.

I’ve always viewed my role within someone’s trust zone as a filter who helps families make sense of the world they are investing and planning in, while deeply understanding their family dynamics, goals, careers, and how it all fits together.

Your trust zone is where your most important financial decisions are made.

Whoever is in that zone, your trust zone, is critical.

So the obvious question is, do you have the right advisor in your trust zone?

Choosing the right advisor is one of the most important financial decisions you will ever make. Most people stay with the same advisor for meaningful parts of their career and life. We have clients who have been with my family for more than forty years.

Here is what matters most for the person who occupies your trust zone with you:

Technical competence

Experience with your specific situation

Shared values

Transparency and aligned incentives

Keep that trust zone idea in your mind as you read these.

1. Technical Competence

Your advisor should be highly skilled in three areas: investment management, tax strategy, and financial planning.

Financial planning is a bit of a catch-all term, but it ties everything together as your wealth grows. From these three areas come what you need most in retirement: consistent income and principal protection on your investments.

An advisor’s ability to integrate all three is what separates good from great. Your financial life is not a set of separate silos. It is an ecosystem designed for one thing: your freedom, and gaining more of it.

2. Experience with Your Situation

You want someone who understands people like you.

For example, I get along with business owners especially well, because I am one. I know what it feels like to balance payroll, manage cash flow, and the constant game of whack-a-mole we all play.

My combination of personal experience and technical skill allows me to serve business owners in a way that goes beyond numbers. I get them and they get me.

I can enter a business owner’s trust zone with personal experience in a way that I simply cannot for let’s say, a physician.

I may understand the financial life of a physician, but I will never understand what it feels like to perform surgery on a living, breathing human being who is scared and thinking of the worst outcome as they drift off under anesthesia.

That’s just not my experience nor my cards in life.

Whatever your situation is, find someone who has deep experience with people like you. They should speak your language and understand the financial realities of your life.

3. Shared Values

When you hire an advisor, you are not just paying for expertise. You are choosing alignment. The trust zone is a sacred place, and you need to be careful about who you let in.

Do they share your values? Do you enjoy the conversation when they call to check in?

I always tell people that if you have two or three advisors who are all technically strong, trustworthy, transparent, and aligned with your values, pick the one you like most.

You should look forward to working on your money with this person, not quietly dread it.

Share values. Build trust.

4. Transparency and Aligned Incentives

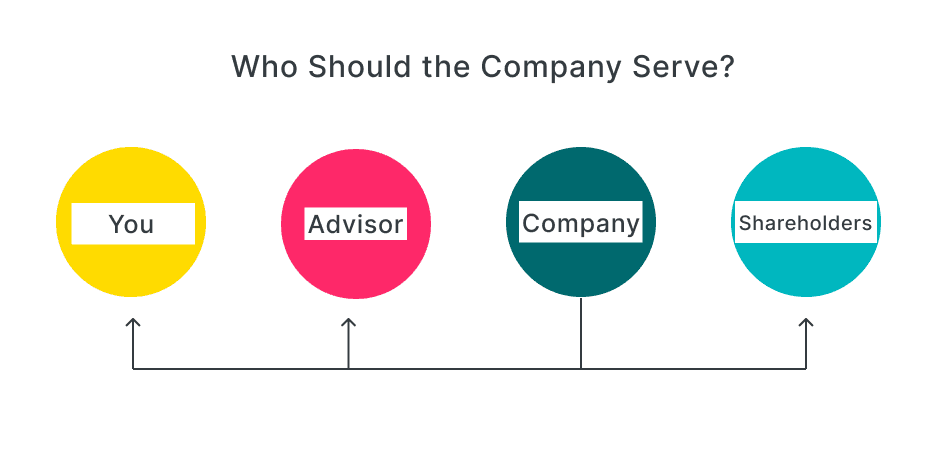

This part is often overlooked. Who your advisor works for, and how they are compensated, shapes the advice you receive.

Here’s how it works:

I have been an advisor at a publicly traded company, a private equity-backed hybrid platform, and now as the owner of an independent, employee-owned firm.

Each place has tradeoffs, but what I will say from my personal experience is that external shareholders, and their timelines, can absolutely move the incentive structure for advisors and affect the experience and advice you receive.

If you advisor works at a large publicly traded company, by no means am I saying you should run for the hills nor am I say that because I run an independently owned SEC-registered investment advisor, we are somehow a perfect solution.

No, what I am saying is you need to understand the incentive structures of where you choose to work.

What I personally believe after working at the three major different types of firms is this: whoever owns the business where your advisor works has a huge influence on your financial life.

Recent example, Edward Jones is not doing alternative investments for clients with less than $10 million, period. The big Wall Street Banks, have been pushing them hard for a broader range of clients.

Who’s right and who’s wrong?

Time will tell, but many clients at Edward Jones don’t even have a choice in the matter.

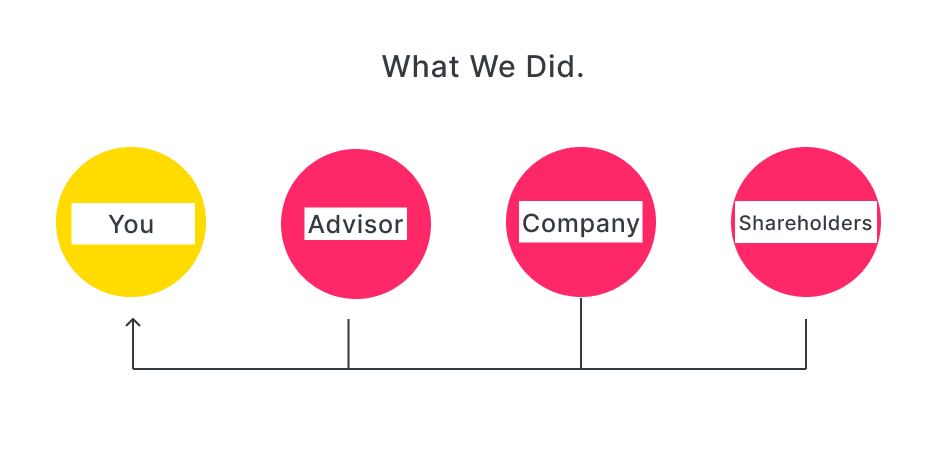

Here’s what we did at Fjell to address this conflict:

We are proudly employee-owned

We are employee-owned.

Our senior advisors who work directly with clients each own part of our company, Fjell.

We are the shareholders, the company, and the advisors. We don’t send quarterly dividends to outside shareholders. We don’t feel the pressure of public earnings calls. And we don’t carve up clients into divisions or territories to maximize profit.

We exist solely to serve our clients. We are not on an artificial timeline driven by private equity or the public markets.

When clients win, we win.

And always in that order.

Your trust zone is sacred ground.

Picking the right financial advisor is about trust, communication, expertise, and alignment.

Great advisors are just that, great.

Bad advisors are just that, bad.

Find someone who communicates clearly and consistently. Someone who understands your situation and has the technical skill to navigate it. Someone who shares your values and has next to no conflicts of interest standing in the way.

The right advisor will be an accelerant to you and your money.

And if you already have an advisor but something feels off, start with a conversation. Sometimes better communication can reignite a great relationship. Other times, it is a sign to bring someone else in.

Either way, be intentional. The world we are living and investing in is changing fast, there are a lot of pressures on your financial life right now, particularly if you are in your 50s and 60s, much of which you don’t even see.

Now is the time to make sure you have the right person in your trust zone.

Thanks for your time this week.

Tom

Want More?

Here are some of our most popular posts.

Retire Wiser

Join the 24,000+ investors who read tmrw each Thursday.